How has net energy metering in California evolved over the last 20 years? This report chronicles the legislative history of net metering in California from its introduction in 1996 to the landmark passing of NEM 2.0 in 2016.

The Golden State for NEM

The Golden State for NEM

Net Energy Metering, or NEM, is a billing system that credits electricity customers for the excess electricity produced by their own generation system (e.g., rooftop solar panels) and sent to the electric grid. NEM was pioneered in the early 80s in Idaho and Arizona, and it was initially passed in California in 1996. The goal of California’s SB 656 legislation was to diversify the energy resource mix, stimulate economic growth in California, and encourage private investment in renewable energy. In that pursuit, NEM legislation has helped California approach its goals; the state is now the leader in residential solar with 2,449 MW of installed capacity as of 2015, more than five times than any other state. Since NEM began in California in 1996, the economics of distributed energy resources (DERs), like rooftop solar, have dramatically improved, increasing participation in NEM. To accommodate the growing demand for NEM—as well as the needs of different NEM stakeholders, including investor-owned utilities (IOUs) and NEM customer generators—California has iterated on its NEM legislation several times over the past 20 years. This process culminated with the creation of NEM 2.0, the program’s most significant change which was passed by the California Public Utility Commission (CPUC) in January 2016.

20 Years of NEM in California

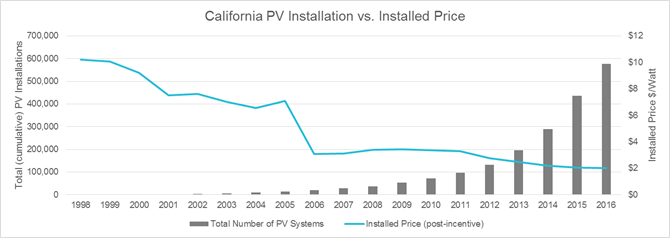

In 1996, SB 656 stipulated that residential customer generators with solar installations of up to 10 kW in capacity could send their excess power to their utility and be credited at the full retail rate (also referred to as net billing). Like the NEM legislation that would follow, the first NEM program set a maximum NEM capacity for which California utilities were required to provide NEM contracts to their customer generators. SB 656 set this maximum to 0.1% of the utility’s peak electricity demand forecast for 1996, which equated to 53.3 MW across the state’s three IOUs. Despite customer generators receiving the full retail rate for their excess power, the high capital costs of rooftop solar systems limited customer generator participation in the earliest NEM program. Since 1996, installation and equipment costs have improved, and federal and state tax incentives have been introduced, including the 30% Federal Investment Tax Credit. Over time, these factors have helped drive down the costs of rooftop solar and increase participation in California’s NEM program (Figure 1).

Figure 1: California Residential PV Installations vs. Installed Price

As participation grew from 1996–2002, California revised the NEM program through four assembly bills to accommodate different distributed generation system types and to raise capacity constraints, sparking exponential growth of participation in the NEM program over the following decade. First, in 1998, AB 1755 expanded NEM-qualifying systems to include small wind installations, and it required utilities to provide a standard NEM contract for all eligible NEM customer generators, two features that continue today. AB 1755 also stated that in these standard NEM contracts, NEM customer generators were to pay the same electricity rates and fees as non-customer generators in their rate class, and they would not be charged the fees that larger power generators were required to pay, including standby charges, demand charges, interconnection fees, and minimum monthly charges. Subsequent rulings continued to protect NEM customers from these additional fees, claiming such charges were “contrary to the intent of this legislation”.

Next, in 2000, AB 918 improved the transparency of the NEM program reporting by requiring utilities to make installed NEM capacity data publicly available. In 2001, AB 29 removed the NEM-installed capacity constraint and increased the individual system size cap from 10 kW to 1 MW, which opened the door for large commercial and industrial customer generators. Passed in 2002, AB 58 was one of the most influential of the early NEM legislation updates. While AB 58 reinstated the NEM-installed capacity constraint, it was the first of many bills to increase the cap, this time from 0.1% of peak capacity to 0.5%. This increased the capacity limit to approximately 270 MW. AB 58 also stipulated that the large systems recently added in AB 29 (systems between 10 kW and 1 MW) would be required to use time-of-use (TOU) rates, as opposed to the standard retail rates. Under this ruling, customer generators received payment for their excess generation relative to the TOU rate, so that the value of the energy provided by the customer generator was aligned to the needs of the grid. Originally, TOU rates were confined to large commercial and industrial customer generators, but this early implementation of TOU rates was a precursor to NEM 2.0, under which all future NEM customer generators will be required to use the TOU rate structure. Finally, AB 58 required the CPUC to examine different methods to ensure that NEM customer generators would not be exempt from non-by-passable charges, like the public purpose charge or charges for recovering bond-related costs. This was new language but consistent with the concept that NEM customer generators be treated like their rate class counterparts. Until the implementation of NEM 2.0, NEM customers received a slight benefit on non-by-passable charges compared to their rate class counterparts, as these volumetric charges were calculated based on a customer’s net energy consumption from the grid, not the total energy consumed from the grid.

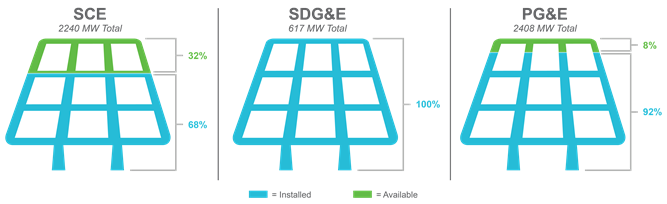

Since AB 58, the NEM program has been updated four more times with the first two updates creating limited changes beyond raising the capacity limits. From 2006–2010, the cap increased from 0.5% to 2.5% through SB 1 and to 5% through AB 510. Furthermore, in 2012 through Decision 12-05-036, the CPUC adopted a new calculation of peak demand. The CPUC’s decision updated the capacity terminology from “aggregate customer peak demand” (interpreted as coincident customer peak demand) to non-coincident customer peak demand, effectively doubling the 5% cap. This decision also required California’s IOUs to report their peak demand calculation and installed capacity yearly. Figure 2 tracks each utility’s progress toward its respective capacity limit over the past four years.

Figure 2: California IOUs – Percentage of NEM Cap

In the 2012 Decision 12-05-036, the CPUC also stated that the NEM program would be suspended in 2014, pending further CPUC proceedings. The introduction of AB 327 in 2013 set the risk of NEM program suspension aside for a few more years by extending the deadline for customer generators to be grandfathered into NEM 1.0 contracts. Under AB 327, NEM applications could qualify for NEM 1.0 contracts if their application was received before their utility reached the statutory net metering cap (5%) or before July 1, 2017, whichever came first. This was a significant extension as the recent growth rate of the NEM program was high—nearly doubling from 2010 to 2012 (660MW to 1,290MW)—and the IOUs were still far from reaching the NEM cap at 1.2% of the 5% cap. Finally, AB 327 qualified energy storage for the NEM program so it would be treated in the same manner as other DERs, like rooftop solar.

While AB 327 helped continue California’s NEM program into 2017, it was designed as a stop-gap legislation for the program. However, AB 327’s lasting impact is seen in the state’s residential rate reform initiative. After the bill’s introduction, the CPUC implemented the law through ruling R.12-06-013, the “Residential Rate Reform Order Instituting Rulemaking,” which aimed to realign rates with several guiding principles that protected ratepayers. To that end, the CPUC passed Decision D.15.07-001 in 2015, providing more specifics on how IOUs could follow the guiding principles introduced in AB 327. These specifics revolved around the consolidation of rate tiers from four to two and the move to TOU rates. This was a double-edged sword for NEM stakeholders; generally, the tier reduction lowered average customer bills, which in turn reduced potential savings (in the form of avoided costs) for customer generators. The decision stands today, and IOUs are required to submit periodic reports detailing their reform progress.

While AB 327 helped continue California’s NEM program into 2017, it was designed as a stop-gap legislation for the program. However, AB 327’s lasting impact is seen in the state’s residential rate reform initiative. After the bill’s introduction, the CPUC implemented the law through ruling R.12-06-013, the “Residential Rate Reform Order Instituting Rulemaking,” which aimed to realign rates with several guiding principles that protected ratepayers. To that end, the CPUC passed Decision D.15.07-001 in 2015, providing more specifics on how IOUs could follow the guiding principles introduced in AB 327. These specifics revolved around the consolidation of rate tiers from four to two and the move to TOU rates. This was a double-edged sword for NEM stakeholders; generally, the tier reduction lowered average customer bills, which in turn reduced potential savings (in the form of avoided costs) for customer generators. The decision stands today, and IOUs are required to submit periodic reports detailing their reform progress.

NEM 2.0: Paradigm (Cost) Shift

On January 28, 2016, the CPUC approved the NEM successor tariff (Decision 16-01-044) or more commonly referred to as NEM 2.0. The ruling confirms the most radical changes to the NEM program since its inception by addressing both fixed fees and repayment rates, as well as by removing the installed capacity constraint which has been a staple of the NEM program since 1996. Some of the major changes under NEM 2.0 include charging new NEM customer generators a one-time interconnection fee between $75–$150 and applying non-by-passable charges (~$0.02/kWh) on the full amount of electricity consumed from the grid (not just net consumption as previously charged). The headline change, though, is the use of default residential TOU rates for all new NEM 2.0 customers, which translates to a decline in average credits for customer generators. Despite some of the increased costs to the customer generators in NEM 2.0, some of the primary benefits of the previous program have remained, including customer generators being provided with the full retail rate for their excess generation and the exemption of standby and fixed charges like demand charges, grid access charges, or installed capacity fees.

NEM 2.0 will only apply to customers who file interconnection applications after the NEM 1.0 ceiling is reached in the applicant’s respective service area or after July 1, 2017, whichever comes first. For SDG&E and PG&E customers, this ceiling has already been reached, and all future NEM applicants in these areas will participate in the NEM 2.0 program. SCE still hasn’t reached its limit, and new NEM applicants will be able to qualify for the NEM 1.0 program until SCE reaches its limit or until July 1, 2017, as stipulated in Decision 16-01-044. Customers who filed before these limits were reached will not be affected by NEM 2.0 and will remain eligible for the NEM 1.0 program for the duration of their system’s contract (typically 20 years).

A Bright Future

Despite the shift of some costs to the NEM customer generator through the NEM 2.0 program, near-term growth is expected to continue and uncertainty about future program changes may drive further participation under the NEM 2.0 program structure. One unknown is how customer behavior may change due to the institution of the new fees and TOU rates. One response could be the increased adoption of new technologies, including battery storage, which will allow customer generators to hold energy collected by their solar panels until the times of day that the energy they produce is most valuable.

NEM 2.0 isn’t changing in isolation; the program is complemented by the CPUC’s DER Action Plan, released in November 2016. The plan’s objectives are to help stakeholders properly value DERs and accelerate the adoption of TOU rate pilot programs. Currently, the CPUC’s focus is on developing a publicly available DER valuation tool with comprehensive location-specific system data. A CPUC-appointed working team has run into issues to date, but there is still optimism that a refined version of the tool will provide an accurate, objective measure of the value of DERs to the distribution system.

The DER Action Plan is a critical step in California’s grid transformation, but it is not a final solution. The plan is mapped out through 2019, a short two years away, when NEM 2.0 is also set to be re-evaluated. NEM 2.0 represents the biggest shift to date, but it is also the culmination of years of legislation, rulemakings, orders, and decisions at the state and commission level. If the next 20 years of NEM in California are anything like the first 20, expect NEM 2.0 to change and change again.

Additional Contributing Authors: Mark Ladisch and Buck Hagood

View MoreSussex Economic Advisors is now part of ScottMadden. We invite you to learn more about our expanded firm. Please use the Contact Us form to request additional information.